The search for income

How clients are seeking new and varied forms of income

Savvy investors have always liked income over capital.

Capital is fixed and can easily be eroded - either by inflation or prolific expenditure. But regular, steady income is essential for people to maintain a certain degree of living.

Without an adequate income, purse-strings must be tightened and financial worries begin to creep in. In the words of Robert Wesley Miller: “When you are not making an income, you must surrender to some outcomes.”

Many people rely on their salary as their principal source of income, but upon this one can add interest on savings, dividends, property rental and yields on bonds, which can help provide a stream of money coming into the household.

However, in this age of ultra-low interest rates on cash, meagre yields on sovereign debt and an uncertain economic outlook for the UK, given the vote to leave the European Union, where can investors go to find such income? Have the streams dried up among UK corporates?

When you are not making an income, you must surrender to some outcomes

According to Nick Kirrage, fund manager for the equity value team at Schroders, there are plenty of opportunities for income-hungry investors, but they just need canny advisers to help them sift the wheat from the chaff.

In his video below, Mr Kirrage discusses where and how good income streams can be sought - but not at any cost.

As he comments, looking for income now among the largest companies and the smaller stocks in the UK is akin to having your “head in the oven and your feet in the fridge”.

In other words, your average temperature may be fine but there are problems at the extremes. Just so it is with UK corporates: the traditionally large, safe players may not be so reliable as a source of income, while the smaller companies issuing big dividends may not continue to deliver.

Simoney Kyriakou is content plus editor for FTAdviser

A bias to growth?

Source: Fotoware

Income investors seem to have a huge bias towards growth at the moment.

Value and growth are often viewed as two sides of the same coin. If your portfolio is 50 per cent in value-oriented investments, it is fair to suggest the other 50 per cent is in growth – or, as they tend to have it in the US, ‘momentum’ – stocks.

If you are 30 per cent in value, then the chances are you are 70 per cent in growth.

If you ask them nicely, the analysts at Morningstar can break down portfolios by investment style and so we asked them to do just that for funds in the UK Income category.

We then made the reasonable assumption that, if a fund has more than 50 per cent in value-oriented stocks, it has a value focus and, if it has more than 50 per cent in growth stocks, it has a growth focus.

Value pretty much embodies everything investors currently find problematic – commodities, banks, volatility and so on

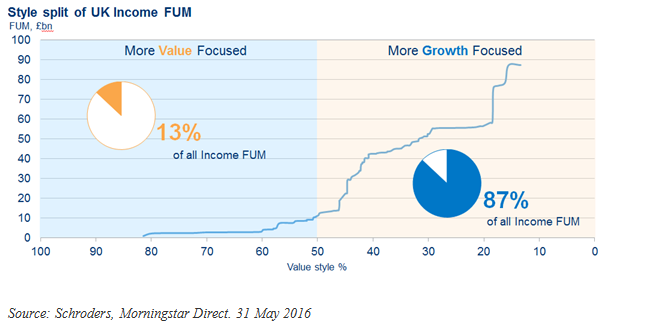

The funds that make up Morningstar’s UK Income sector boast a chunky £87bn in assets under management.

We disaggregated this figure into the percentage value run by each investment house and then ranked everything according to the degree to which they are focused towards value or growth.

The resulting chart (right) paints an arresting picture.

As you can see, 87 per cent of all £87bn of funds under management in the UK Income sector have a greater than 50 per cent bias to growth, which of course means just 13 per cent have any sort of tilt towards value.

Prominent in the former camp is the vertical line towards the right of the chart, which represents the £18bn one investment house has across its stable of growth-oriented income portfolios.

Towards the left of the chart, the great majority of the £5bn or so of assets with a 60 per cent or higher tilt towards value are also run by a single investment house.

We presume its identity goes without saying and so will instead concentrate on what this chart is saying – most obviously that, as things stand, almost nobody wants to touch value.

That is because value pretty much embodies everything investors currently find problematic – commodities, banks, volatility and so on.

In contrast, growth is a much easier decision for investors – at least at first glance – and there is certainly no denying a lot of the funds that make up the right-hand side of our chart can point to excellent 10-year track records.

Yet we know markets are cyclical over time. We know businesses and sectors – whether they have been doing well or poorly – revert to the mean over time. And we know that – again, over time – value has a long, long history of outperforming growth.

All of which means the funds on the right-hand side of the chart – and their investors – represent a strong bet against history repeating itself. Over time.

The chart also has us wondering about the way many investors will say they like to diversify their income exposure by blending together different funds with different holdings.

Well, of course that is possible but investors taking this approach with UK equity income funds might want to revisit just how diversified they currently are.

Certainly, if you were to pick two funds at random from the UK Income sector today, with a view to blending them together, the odds strongly suggest you would end up with two portfolios of very similar stocks and not a great deal of genuine diversification. You would only achieve that by blending two funds with different investment styles.

As keen commentators of behavioural finance it does not come as much of a surprise to see such a huge bias to the investment style that has performed so well over the last decade or so.

Of more interest to us, however, is the huge risk we believe this positioning now poses to the great majority of investors in the sector – and the great opportunity it presents to our own investors.

Nick Kirrage is fund manager, equity value, for Schroders.

Where are advisers looking?

Source: Fotoware

Post-Brexit vote, it seems advisers have been heading overseas for good equity income stocks for their dividend-hungry clients.

According to research from The Share Centre, second quarter underlying dividends in the UK were the weakest performers among the Group of Seven leading industrialised nations.

Spates of cuts to dividends came as UK companies stopped spending more on dividends than they made in profits, as they reinvested into their business.

Moreover, the US and Japan are both looking more promising. For example, 49 per cent of the S&P 500’s constituents yield in excess of 2 per cent, while commentators have been speculating that the good health of Japanese corporates may manifest itself in higher dividend payouts over the coming months.

These may be reasons why advisers have been seeking overseas equity income yields for their clients.

A poll carried out by FTAdviser Talking Point during September revealed 50 per cent of advisers believed the best income streams were coming from overseas equity income.

UK investors have grown accustomed to companies slashing payouts

Only 25 per cent believed UK equity income was still offering the best value and prospects for dividend growth.

Yet Nick Kirrage, co-head of Schroders global value equity team issues a word of caution about chasing yields for the sake of it.

He says: "Everyone is looking for income, aren't they? It seems to be the answer to every question in the investment industry: 'How do I get income? Where do I find it?'

"Equity income, of course, is a valid place to be looking for that. But when everyone wants the same thing, it tends to get expensive. This is an issue."

He added that, while seeking this sort of income stream, people do not want to hurt their capital and overpay for the yield they are chasing.

Indeed, Laith Khalaf, investment specialist for Hargreaves Lansdown, believes there is still plenty of value in UK corporates, and that investors are not too worried by a slight slowdown in dividend rises.

He said UK investors had "grown accustomed to companies slashing payouts" and that axing dividends was “part and parcel of income investing”.

He believes there are still good equity income prospects to be had in the UK. Likewise, SVS Church House Equity Income Fund claimed August was fairly quiet but there were good bargains to be had among UK dividend payers.

According to the fund managers' latest factsheet: "Equities generally held on to their post-Brexit gains.

"The fund had a quiet, yet positive, month. We added to our position to Clinigen, the pharmaceutical company."

Recent flows into fixed-income have been motivated by a global flight to safety after the UK’s Brexit vote

Yet it is not just equity income that is attracting yield-hungry investors; overseas fixed income has also been driving investor behaviour.

According to data from fund analysts Morningstar, fixed income funds saw a strong intake of money during August, as investors withdrew from equity funds and placed money into corporate bond funds.

Matias Möttölä, senior manager and research analyst for Morningstar, commented: "The breadth of investor interest in fixed-income funds in August was such that 71 of Morningstar’s 93 European fixed-income categories saw inflows during the month.

"Recent flows into fixed-income have been motivated by a global flight to safety after the UK’s Brexit vote and also by rising expectations of continued low rates and further extraordinary measures by central banks to accommodate growth in the global economy.

"At the same time, investors continued to withdraw from active equity funds, despite generally positive returns for stocks during the month.”

Simoney Kyriakou is content plus editor for FTAdviser

CPD: The search for income

Source: Fotoware